Having trouble in balancing trial balance? Or got payment but don’t know by whom? Or for what? Are you also stuck between these complications and looking for a way out of them? No worries, the suspense account has a solution for you, but don’t forget it’s a temporary solution you have to resolve it and identify the unclassified transaction as soon as possible.

So, let’s see how the creation of a suspense account will help you to solve your problem.

What Is A Suspense Account?

In This Article

ToggleA suspense account is a temporary account to record an anonymous transaction. In other words, when you don’t have sufficient information; about where to record that particular transaction, you use that account. Moreover, It also helps you balance your trial balance.

- The account works as a temporary solution where you hold an entry that you can’t classify or don’t know where to record.

How Does A Suspense Account Work?

A Suspense account is used in the case of having an unidentified transaction (You don’t know in which account the transaction should be recorded, what is its debit and credit?). Here you go, You record that anonymous transaction into this account. As soon as that unidentified transaction becomes identified, you record them in their respective accounts. Specifically, in accounting, you can use it in two scenarios:

- The difference in trail balance: In this case, the account may be opened with the same amount so that it equalizes the debit or credit side.

- Unable to classify an accounting entry: When the original account is unsure where to post the amount and post it to the account till further instructions.

In accounting two most important things are timeliness and accuracy. All the accounting procedures revolve around it. Most importantly suspense account fulfills your demand for time management. But accuracy remains questioned. In order to fulfill the demand for accuracy, you must search for the errors and remove them as soon as possible. This will make your data accurate.

The problem arises when you leave the amount in a suspense account for so long. With the passage of time, it becomes difficult to clear out errors. Therefore it is necessary to investigate and make corrections on regular basis.

Types Of Suspense Account Errors – When to Use it?

There are different errors that occur during the accounting process. But success is to get out of those errors without being panic. To remove errors we use a suspense account.

Compensating Error: For example, one of your customers pays you but the cashier forgets the name of the customer. You don’t know who has made the payment, therefore, whose account should be credited? In this case, you temporarily create the account in order to balance your trial balance.

For this purpose, cash is debited by 500 and the suspense account is credited by the same amount. Because cash is an asset and an increase in assets is debited.

| Date | Particulars | Dr. | Cr. |

| xxx | Cash | $500 | |

| Suspense Account | $500 |

Besides this situation, there are some other situations in which we create and record transactions into the account.

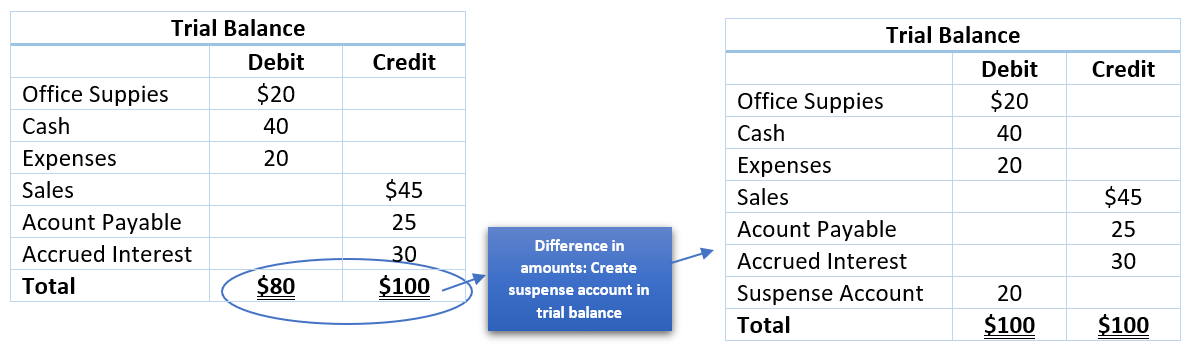

Trial Balance Error: For example, in a trial balance, there are two sides debit and credit if the balance of the debit and credit side is not equal. Create a suspense account in the trial balance to place that debit and credit difference. For instance, you have $100 on the credit side and $80 on the debit side. So, the account would be debited by $20.

The error of omission: In this situation, you can see that the amount in the trial balance is equal. In this case, you mistakenly omit an entry completely. In simple words, you forget to record an entry. Neither the debit nor credit side of the entry is recorded. As a result, both the credit and debit sides will become weaker with the same amount. So, in this case, a suspense account is not created.

The Accounting Procedure

Account Opening

Have an imbalance trial balance? Got anonymous payment? Have to pay for something but don’t know why? Are you facing such complications during your accounting procedure?

You open a suspense account whenever you face the above-mentioned questions. Let’s understand it with the help of examples. For instance, you receive a payment of $300, but who made the payment? Or from where this amount is coming is yet to be known. At that time you are required to open up the account for that specific period in order to balance your trial balance. It remains open till the error is found.

Once the error is found you close the account. To open it you debit or credit the account as needed. Let’s assume the debit side of your trial balance goes higher than the credit side, the difference is recorded as a credit to the suspense account.

Contrarily if the credit side of your trial balance is larger than the debit side, the difference is recorded as a debit to the account.

Account Closing

Open up a suspense account? Thinking that you have got rid of the problem? No, as long as the error is not found you can’t relax.

In accounting not only timeliness is important. As far as the accuracy of data is concerned it is equally important. Hence it is necessary to locate errors and make corrections. The account is closed as soon as the error is discovered.

Suspense Account Example

Let’s have a deep look into some examples to get a more clear picture of how an error is found and eventually removed. For instance, you receive a payment of $200 from a customer. But you don’t know who made this payment.

As we don’t know who has made the payment therefore we debit to cash and credit suspense account. If we knew who has made the payment then that person’s account would be credited.

Suspense account journal entry:

| Date | Particulars | Dr. | Cr. |

| xxx | Cash | $200 | |

| Suspense Account | $200 |

So in order to find out the error, you can match the amount in payment with the invoice that you sent to your customers. Furthermore, once you match the payment you must also contact the respective customer and make sure that he/she has made this payment or not.

Once the error is found, the inquiry is made. You will take out the amount from the suspense account and credit the customer’s account. You make corrections and finally dispose of the account. The sooner you find out the error the quicker your accounting process becomes accurate.

| Date | Particulars | Dr. | Cr. |

| xxx | Suspense Account | $200 | |

| Account Receivable- Mr. John | $200 |

Suspense Account Debit or Credit: In some novel cases, you can’t find the error. Therefore, if the amount in the account is debit you record it on the asset side of the balance sheet. Similarly, if the amount in the account is credit, it will be recorded in the liabilities portion of the balance sheet.

Key Points

- A suspense account is a temporary and an error remover account.

- In accounting processing, you can use this account in two scenarios: in trail balance error and when unable to classify a transaction or entry.

- A suspense account is always made on the weaker side of the trial balance.

- It cant be made as long as debit and credit are equal.